Welcome to the quantitative side of Polymarket. If you are reading this, you understand that predicting the future is difficult, but capturing mathematical inefficiencies in real-time order books is highly replicable.

This tutorial is broken down into the three dominant arbitrage vectors currently active in 2026. We will cover the specific theory, the implementation mechanics, and the necessary tools to automate the workflow.

Vector 1: Mathematical Spreads: Kalshi vs Polymarket API

The Core Mathematics

Prediction markets use a binary $0.00 to $1.00 pricing model, where the price perfectly correlates to the market-implied probability of an event. A "Synthetic Hedge Gap" occurs when you can purchase 100% of the outcome space for less than $1.00 across platforms.

Platform Discrepancies: Kalshi vs. Polymarket

Because Kalshi explicitly serves US-verified retail liquidity while Polymarket relies heavily on crypto-native global liquidity, their pricing graphs frequently disconnect during high-volatility news events.

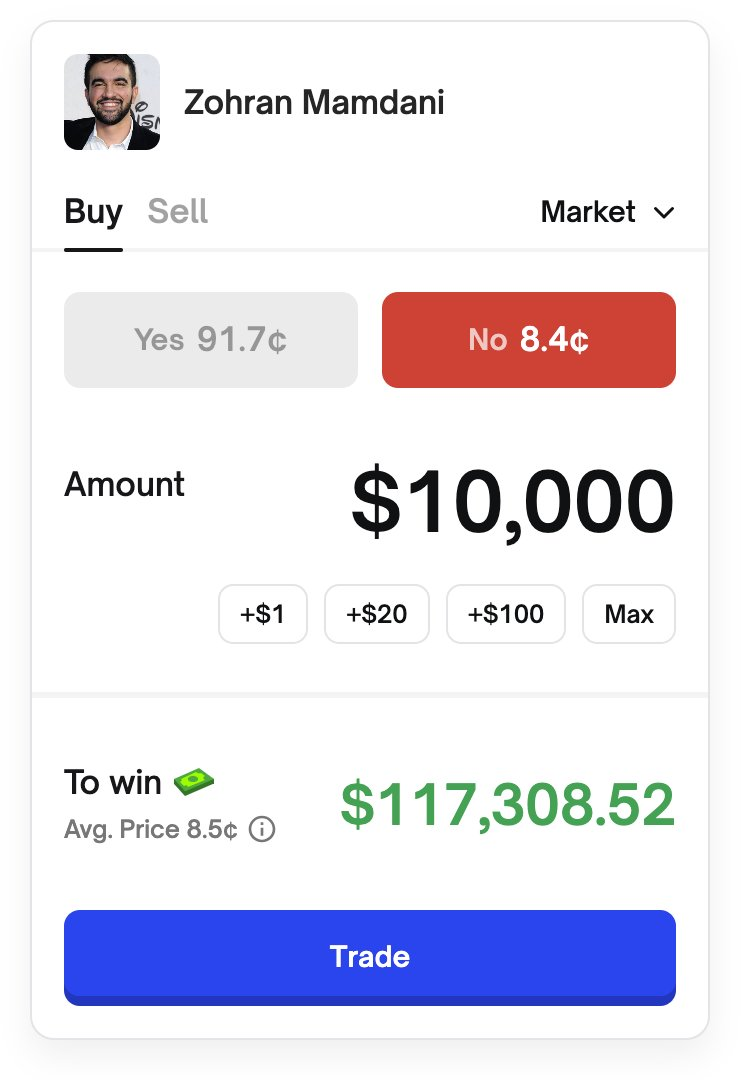

Pricing on US-Regulated Kalshi

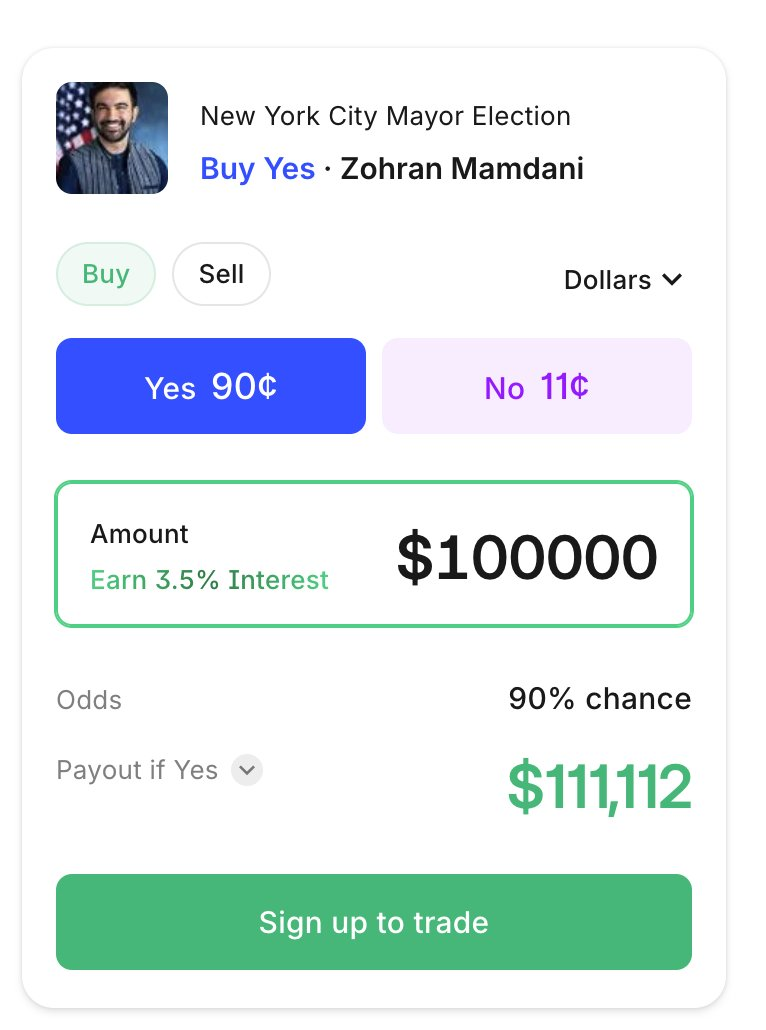

Pricing on Crypto-Native Polymarket

Vector 2: Latency Arbitrage: Beating Retail to Whale Sweeps

Finding cross-platform spread discrepancies manually is physically impossible; by the time your browser renders the Kalshi DOM and the Polymarket DOM, trading algorithms have already filled the arbitrage gap.

The same applies to tracking "Whale Sweeps". A whale sweep is when a massive wallet unloads a $100k+ market-buy into the order book, creating a cascading price spike. Capturing the remaining tail-end liquidity before the market corrects is highly profitable but requires API-level speed.

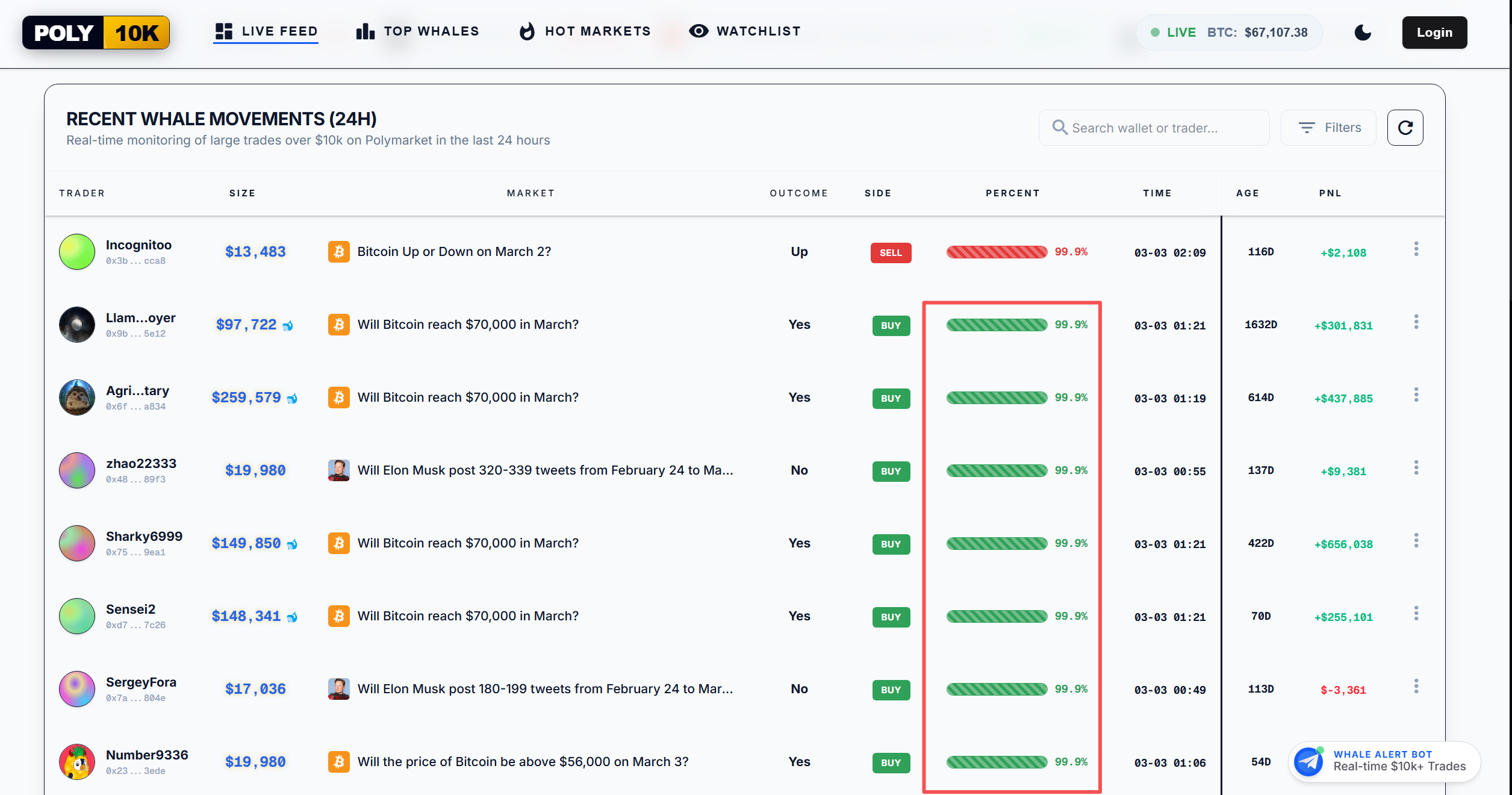

Integrating The Poly10K Tracking Platform

To solve this, professional traders utilize the Poly10K Tracking Platform. Our custom-built monitor scans the Polymarket Polygon contract for specific transaction sizes and emits WebSocket alerts.

The Poly10K UI visualizing a massive sweep.

Actionable Workflow:

- Create an account on www.poly-whale.com to tap into the WebSocket stream.

- Configure your alert thresholds (e.g., Only alert when Taker Volume > $25,000 within a 1-minute window).

- When the alert fires, evaluate the remaining order book depth for the opposite side of the trade, as automated market makers will scramble to rebalance.

Vector 3: Delta-Neutral Yield Farming Math

If you don't want to build API integrations, becoming a structural Maker is your most viable quantitative arbitrage route.

Polymarket's reward algorithm uses a continuous snapshot mechanism to distribute USDC to users maintaining limit orders near the spread. The formula penalizes distance from the midpoint quadratically.

The "Two-Sided" Execution:

To remain delta-neutral, you must provide liquidity to practically impossible markets (where probabilities are < 2%). By placing limit orders on both the YES and NO side of an extremely illiquid contract bearing the "$ Reward" icon, you harvest the hourly USDC snapshot distributions with minimal risk of your orders being filled. If one side is miraculously filled, you immediately cancel the opposite side and swallow the nominal loss, compensated by days of prior reward farming.

Conclusion

Arbitrage on Polymarket is no longer a manual game. Rely on infrastructure like Poly10K, understand the math behind quadratic rewards, and view every order book merely as an equation of `$1.00 - (YES + NO)`.